Quick Guide to ensembleHTE

Bruno Fava

2026-05-22

Source:vignettes/getting-started.Rmd

getting-started.RmdIntroduction

The ensembleHTE package provides tools for learning

features of heterogeneous treatment effects in randomized controlled

trials using an ensemble approach. The package implements the estimation

strategy developed in Fava (2025), which combines predictions from

multiple machine learning algorithms using Best Linear Predictor (BLP)

weights and repeated K-fold cross-fitting.

Key Concepts

GATES (Group Average Treatment Effects)

GATES provide a way to test for and visualize treatment effect heterogeneity by:

- Using machine learning to predict individual treatment effects based on covariates

- Sorting individuals into groups (e.g., terciles) based on these predictions

- Estimating the average treatment effect within each group

- Testing whether high-prediction and low-prediction groups have different effects

The Ensemble Approach

This package improves upon existing approaches by:

- Combining Multiple ML Algorithms: Combines predictions from several algorithms (Random Forest, XGBoost, etc.) using BLP weights

- K-fold Cross-Fitting: Trains models on K-1 folds and predicts on the held-out fold

- Full-Sample Inference: Uses the entire dataset for final estimation

- Repeated Sample-Splitting: Averages across M repetitions for stability

Basic Workflow

1. Load Data

We use the microcredit dataset that ships with the

package. It contains data from a randomized microfinance experiment in

the Philippines where microloans were randomly offered to

applicants.

library(ensembleHTE)

data(microcredit)

dim(microcredit)

#> [1] 1113 51

# Variables used throughout this guide

hte_covars <- c("css_creditscorefinal", "own_anybus",

"max_yearsinbusiness", "css_assetvalue")

has_loan <- microcredit$treat == 1 & microcredit$loan_size > 0

# Income quintiles (used for restricted comparisons)

microcredit$hhinc_quintile <- cut(

microcredit$hhinc_yrly_base,

breaks = quantile(microcredit$hhinc_yrly_base, probs = seq(0, 1, by = 0.2)),

labels = paste0("Q", 1:5),

include.lowest = TRUE

)2. Fit Ensemble HTE Model

We test whether the effect of being offered a microloan on business expenses varies across borrowers.

# Select covariates

hte_covars <- c("css_creditscorefinal", "own_anybus",

"max_yearsinbusiness", "css_assetvalue")

# Fit ensemble HTE model

fit <- ensemble_hte(

Y = "exp_yrly_end",

D = "treat",

X = hte_covars,

data = microcredit,

prop_score = "prop_score",

algorithms = c("lm", "grf"),

M = 10, # Use M >= 100 for final results

K = 4

)

# View results

print(fit)

summary(fit)#> Ensemble HTE Fit

#> ================

#>

#> Call:

#> ensemble_hte(data = microcredit, Y = "exp_yrly_end", X = hte_covars_quick,

#> D = "treat", prop_score = "prop_score", M = 2, K = 4, algorithms = c("lm",

#> "grf"))

#>

#> Data:

#> Observations: 1113

#> Targeted outcome: exp_yrly_end

#> Treatment: treat

#> Covariates: 4

#>

#> Model specification:

#> Algorithms: lm, grf

#> Metalearner: R-learner

#> Task type: regression (continuous outcome)

#> R-learner method: grf

#>

#> Split-sample parameters:

#> Repetitions (M): 2

#> Folds (K): 4

#> Ensemble strategy: cross-validated BLP

#> Ensemble folds: 5

#> Covariate scaling: enabled

#> Hyperparameter tuning: disabled

#> Ensemble HTE Summary

#> ====================

#>

#> Call:

#> ensemble_hte(data = microcredit, Y = "exp_yrly_end", X = hte_covars_quick,

#> D = "treat", prop_score = "prop_score", M = 2, K = 4, algorithms = c("lm",

#> "grf"))

#>

#> Outcome: exp_yrly_end

#> Treatment: treat

#> Observations: 1113

#> Repetitions: 2

#>

#> Best Linear Predictor (BLP):

#> beta1 (ATE): -2580.30 (SE: 4397.19, p: 0.557)

#> beta2 (HET): 0.67 (SE: 0.30, p: 0.026) *

#> -> Significant heterogeneity detected (p < 0.05)

#>

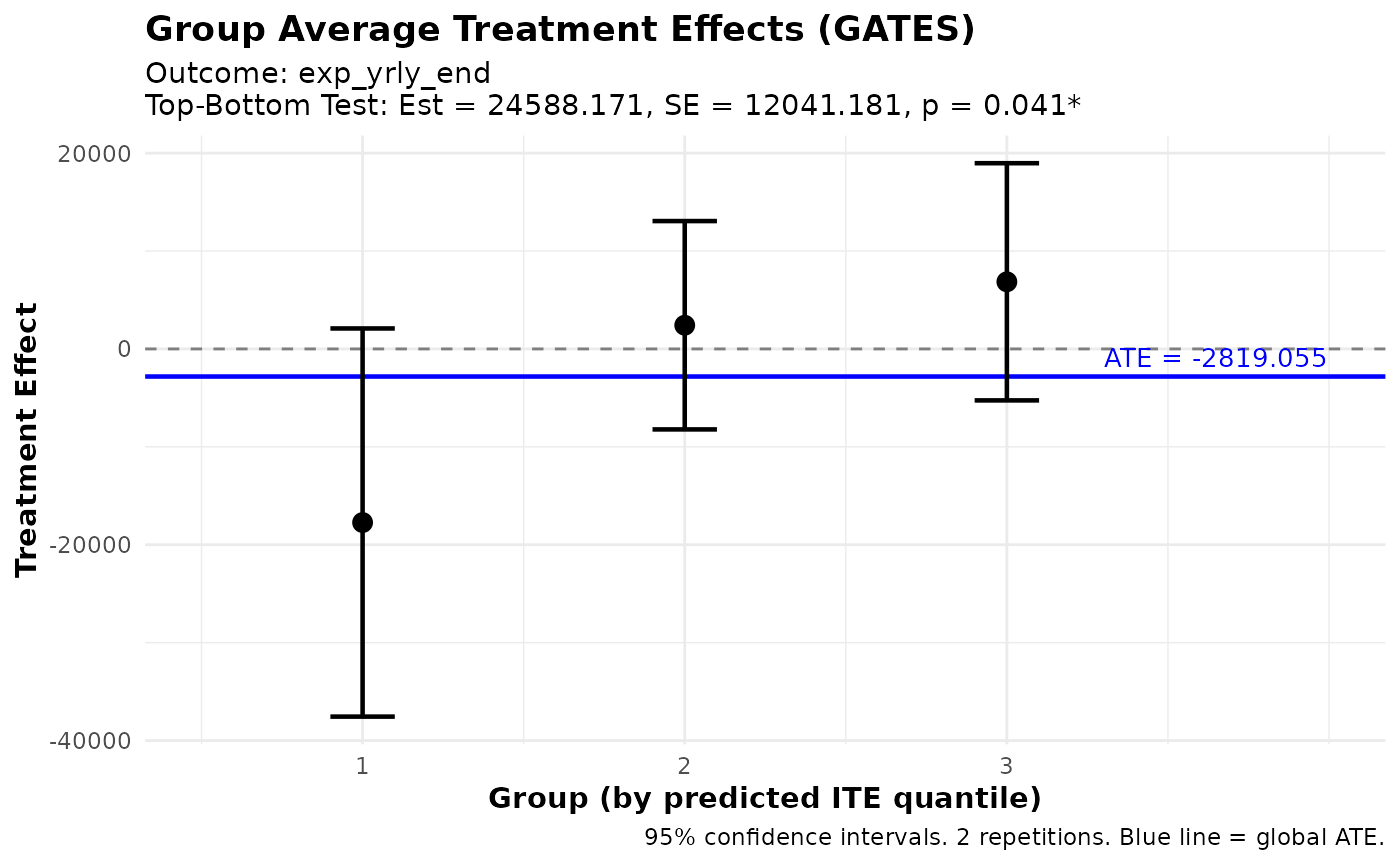

#> Group Average Treatment Effects (GATES) with 3 groups:

#> Group Estimate Std.Error Pr(>|t|)

#> --------------------------------------------

#> 1 -17732.19 10113.66 0.080 .

#> 2 2419.04 5428.34 0.656

#> 3 6855.98 6179.99 0.267

#>

#> Top - Bottom: 24588.17 (SE: 12041.18, p: 0.041) *

#>

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 13. Analyze Treatment Effect Heterogeneity

# Best Linear Predictor (BLP)

blp_results <- blp(fit)

print(blp_results)

#> BLP Results (Best Linear Predictor of CATE)

#> ============================================

#>

#> Fit type: HTE (ensemble_hte)

#> Outcome analyzed: exp_yrly_end

#> Repetitions: 2

#>

#> Coefficients:

#> beta1 (ATE): Average Treatment Effect

#> beta2 (HET): Heterogeneity loading (significant = ML captures heterogeneity)

#>

#> Term Estimate Std.Error t value Pr(>|t|)

#> ----------------------------------------------------

#> beta1 -2580.30 4397.19 -0.59 0.557

#> beta2 0.67 0.30 2.23 0.026 *

#>

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

# Group Average Treatment Effects (GATES)

gates_results <- gates(fit, n_groups = 3)

print(gates_results)

#> GATES Results

#> =============

#>

#> Fit type: HTE (ensemble_hte)

#> Outcome analyzed: exp_yrly_end

#> Number of groups: 3

#> Repetitions: 2

#>

#> Group Average Treatment Effects:

#>

#> Group Estimate Std.Error t value Pr(>|t|)

#> ----------------------------------------------------

#> 1 -17732.19 10113.66 -1.75 0.080 .

#> 2 2419.04 5428.34 0.45 0.656

#> 3 6855.98 6179.99 1.11 0.267

#>

#> Heterogeneity Tests:

#> ----------------------------------------------------

#> Test Estimate Std.Error t value Pr(>|t|)

#> ----------------------------------------------------

#> Top-Bottom 24588.17 12041.18 2.04 0.041 *

#> Top-All 9693.14 5759.59 1.68 0.092 .

#>

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

plot(gates_results)

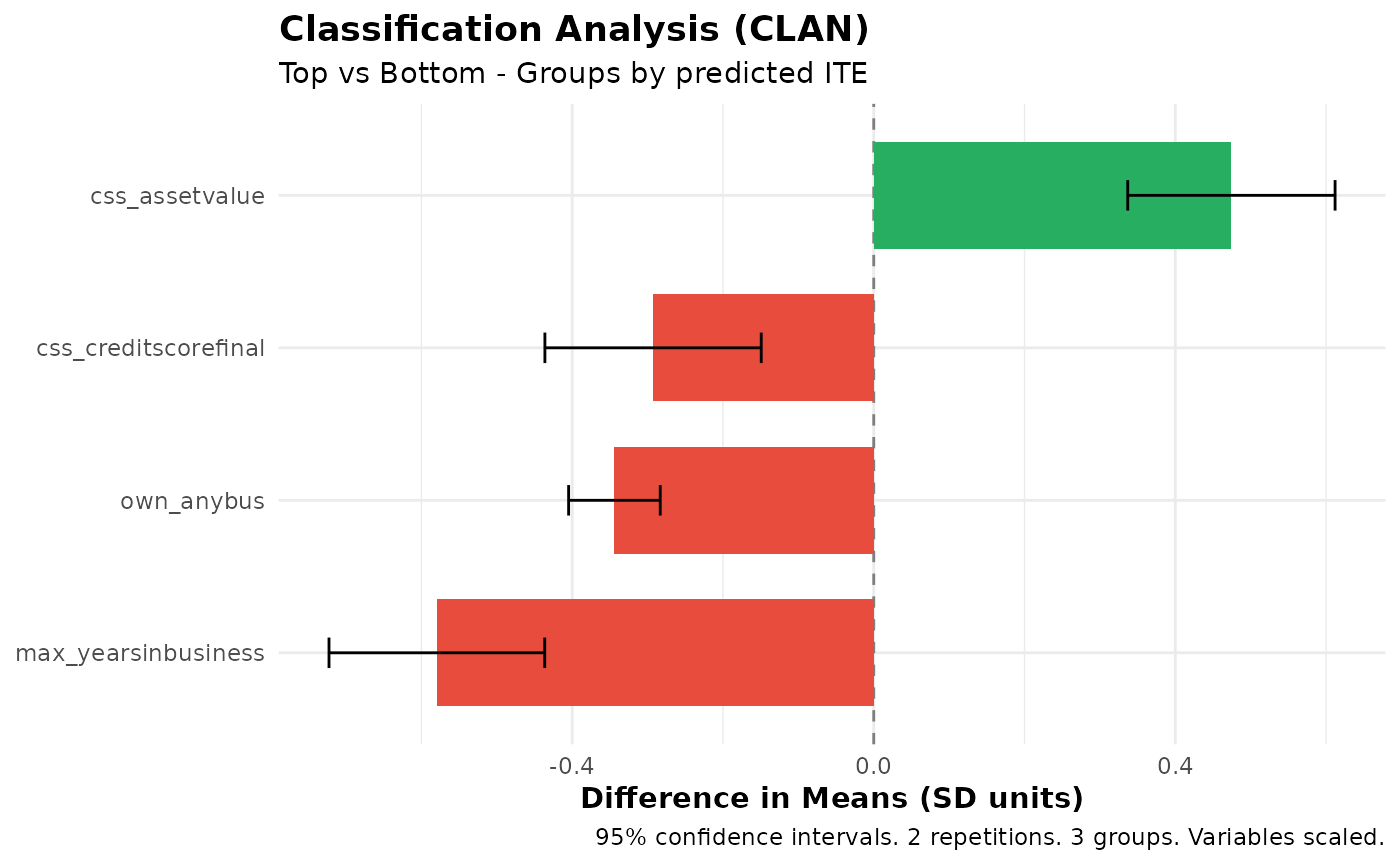

# Classification Analysis (CLAN)

clan_results <- clan(fit, n_groups = 3)

print(clan_results)

#> CLAN Results (Classification Analysis)

#> =======================================

#>

#> Outcome: exp_yrly_end (treatment effects) | Groups: 3 | Reps: 2

#>

#> Group Means (by predicted ITE):

#> Top Bottom Else All

#> --------------------------------------------------------------------

#> css_creditscorefinal 50.51 52.08 51.72 51.32

#> (0.27) (0.29) (0.20) (0.16)

#> own_anybus 0.53 0.88 0.83 0.73

#> (0.03) (0.02) (0.01) (0.01)

#> max_yearsinbusiness 5.16 8.36 7.41 6.66

#> (0.22) (0.34) (0.22) (0.17)

#> css_assetvalue 109209.74 31013.42 44485.77 66060.43

#> (10819.81) (4083.34) (4737.52) (4940.35)

#>

#> Differences from Top Group:

#> Top-Bot Top-Else Top-All

#> -----------------------------------------------------------

#> css_creditscorefinal -1.57*** -1.21*** -0.81***

#> (0.39) (0.33) (0.22)

#> own_anybus -0.34*** -0.30*** -0.20***

#> (0.03) (0.03) (0.02)

#> max_yearsinbusiness -3.20*** -2.25*** -1.50***

#> (0.40) (0.31) (0.21)

#> css_assetvalue 78196.32*** 64723.97*** 43149.31***

#> (11565.28) (11891.83) (7980.06)

#>

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

plot(clan_results)

Prediction Tasks

The package also supports standard prediction tasks (without treatment effects). Here we predict bank profitability per peso lent, training only on borrowers who actually took a loan (where bank profits are observed):

# Identify borrowers with observed bank profits

has_loan <- microcredit$treat == 1 & microcredit$loan_size > 0

# Fit ensemble prediction model

pred_fit <- ensemble_pred(

Y = "bank_profits_pp",

X = c("css_creditscorefinal", "own_anybus", "css_assetvalue",

"age", "gender", "hhinc_yrly_base"),

data = microcredit,

train_idx = has_loan,

algorithms = c("lm", "grf"),

M = 10, K = 4

)

# Analyze predictions

summary(pred_fit)

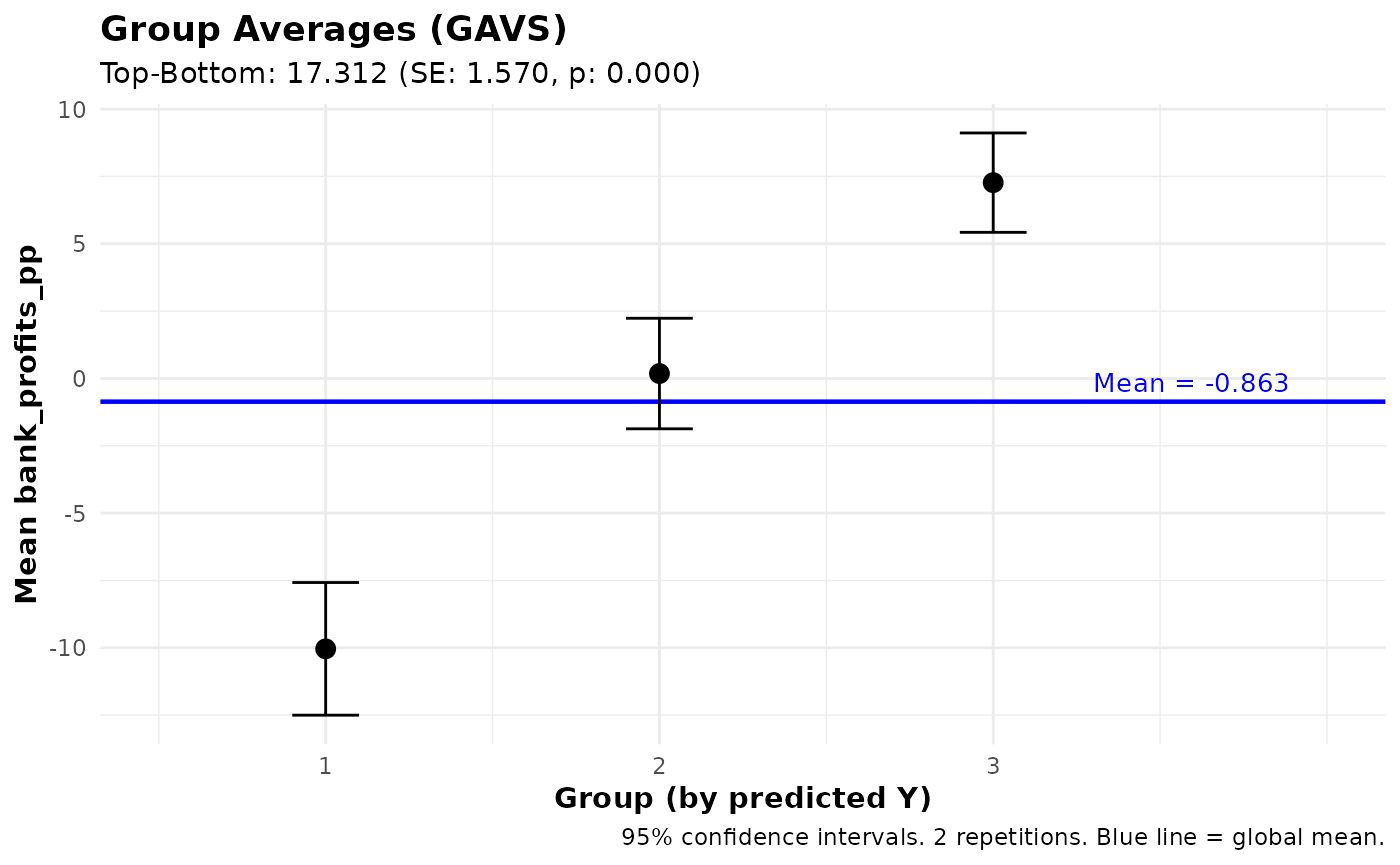

# Group Averages

gavs_results <- gavs(pred_fit, n_groups = 3)

print(gavs_results)

plot(gavs_results)#> Ensemble Prediction Summary

#> ===========================

#>

#> Call:

#> ensemble_pred(data = microcredit, Y = "bank_profits_pp", X = c("css_creditscorefinal",

#> "own_anybus", "css_assetvalue", "age", "gender", "hhinc_yrly_base"),

#> train_idx = has_loan, M = 2, K = 4, algorithms = c("lm",

#> "grf"))

#>

#> Outcome: bank_profits_pp

#> Observations: 1113

#> Training obs: 650

#> Repetitions: 2

#>

#> Prediction Accuracy (averaged across 2 repetitions):

#> R-squared: 0.21

#> RMSE: 15.23

#> MAE: 10.96

#> Correlation: 0.46

#>

#> Best Linear Predictor (BLP):

#> intercept: 0.00 (SE: 0.60, p: 0.995)

#> slope: 0.98 (SE: 0.07, p: 0.000) ***

#> -> Intercept close to 0 and slope close to 1 indicate good calibration

#>

#> Group Averages (GAVS) with 3 groups:

#> Group Estimate Std.Error Pr(>|t|)

#> --------------------------------------------

#> 1 -10.04 1.26 0.000 ***

#> 2 0.18 1.05 0.862

#> 3 7.27 0.94 0.000 ***

#>

#> Top - Bottom: 17.31 (SE: 1.57, p: 0.000) ***

#>

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> GAVS Results (Group Averages)

#> =============================

#>

#> Outcome analyzed: bank_profits_pp

#> Number of groups: 3

#> Repetitions: 2

#>

#> Data usage:

#> ML trained on: 650 of 1113 obs

#> Analysis evaluated on: 650 of 1113 obs

#> Groups (3) formed on: all observations (1113 obs)

#>

#> Group Average Outcomes (groups by predicted Y):

#>

#> Group Estimate Std.Error t value Pr(>|t|)

#> ----------------------------------------------------

#> 1 -10.04 1.26 -7.99 0.000 ***

#> 2 0.18 1.05 0.17 0.862

#> 3 7.27 0.94 7.72 0.000 ***

#>

#> Heterogeneity Tests:

#> ----------------------------------------------------

#> Test Estimate Std.Error t value Pr(>|t|)

#> ----------------------------------------------------

#> Top-Bottom 17.31 1.57 11.03 0.000 ***

#> Top-All 7.28 0.78 9.35 0.000 ***

#>

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

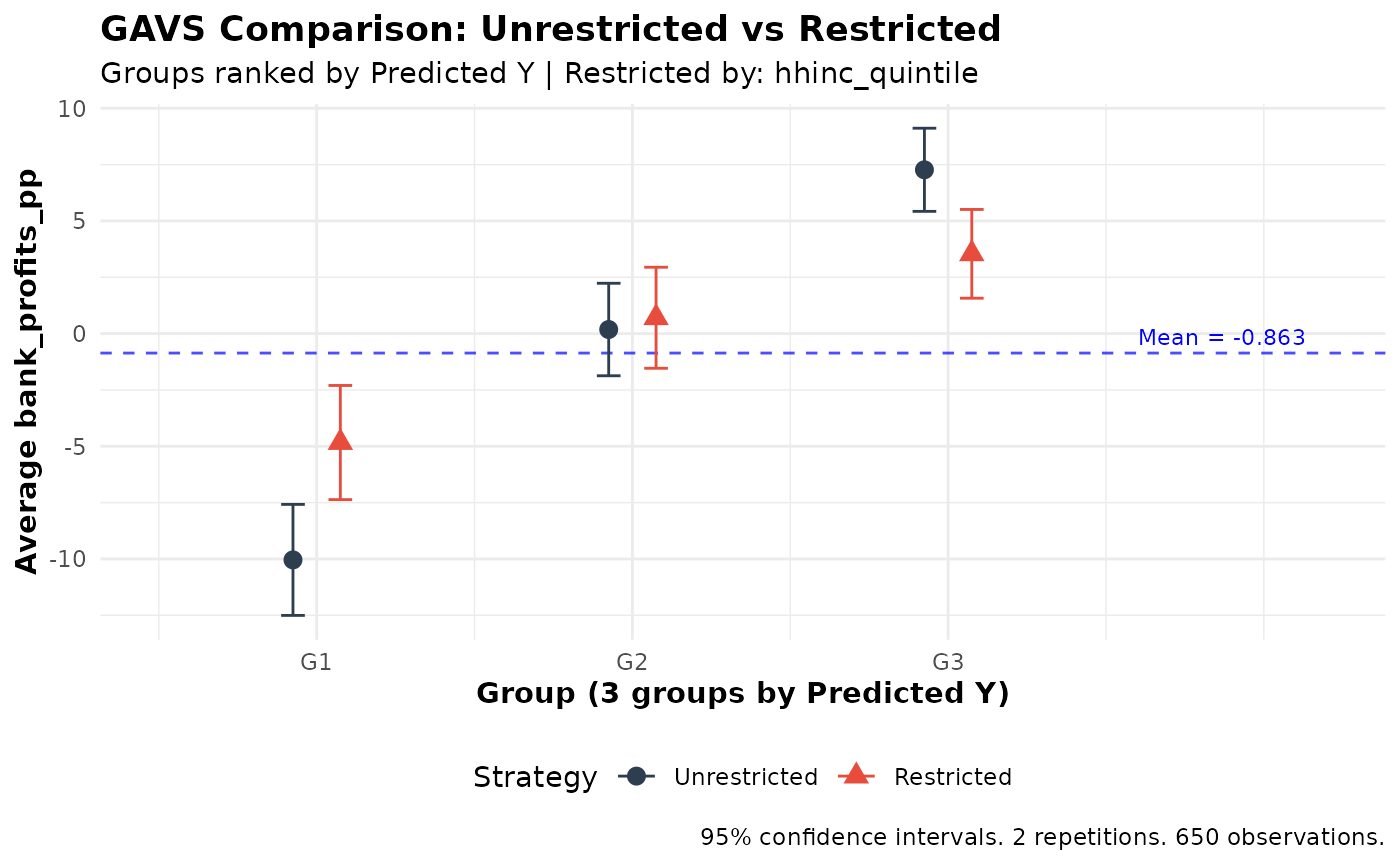

Comparing Ranking Strategies

Use gates_restricted() or gavs_restricted()

to compare unrestricted vs. restricted ranking. Here we test whether

requiring income-balanced loan allocation reduces the lender’s ability

to identify profitable borrowers:

# Compare targeting strategies

comparison <- gavs_restricted(

pred_fit,

restrict_by = "hhinc_quintile",

n_groups = 3,

subset = "train"

)

print(comparison)

#>

#> GAVS Comparison: Unrestricted vs Restricted Ranking

#> ====================================================

#>

#> Strategy comparison:

#> - Unrestricted: Rank predictions across full sample within folds

#> - Restricted: Rank predictions within groups ('hhinc_quintile')

#> - Restrict_by levels: Q1, Q2, Q3, Q4, Q5

#>

#> Groups (3) defined by: predicted Y

#> Outcome: bank_profits_pp

#> Observations: 650

#> Repetitions: 2

#>

#> Unrestricted GAVS Estimates:

#> ----------------------------------------

#> Group Estimate SE t p-value

#> 1 -10.04 1.26 -7.99 0.000 ***

#> 2 0.18 1.05 0.17 0.862

#> 3 7.27 0.94 7.72 0.000 ***

#>

#> Top-Bottom: 17.31 (SE: 1.57, p = 0.000) ***

#> All: -0.01 (SE: 0.62, p = 0.989)

#> Top-All: 7.28 (SE: 0.78, p = 0.000) ***

#>

#> Restricted GAVS Estimates:

#> ----------------------------------------

#> Group Estimate SE t p-value

#> 1 -4.83 1.29 -3.74 0.000 ***

#> 2 0.70 1.14 0.61 0.539

#> 3 3.54 1.00 3.52 0.000 ***

#>

#> Top-Bottom: 8.37 (SE: 1.64, p = 0.000) ***

#> All: -0.01 (SE: 0.66, p = 0.990)

#> Top-All: 3.55 (SE: 0.86, p = 0.000) ***

#>

#> Difference (Unrestricted - Restricted):

#> ----------------------------------------

#> Group Estimate SE t p-value

#> 1 -5.21 1.23 -4.24 0.000 ***

#> 2 -0.52 1.35 -0.39 0.698

#> 3 3.73 1.00 3.74 0.000 ***

#>

#> Top-Bottom Diff: 8.94 (SE: 1.65, p = 0.000) ***

#> All Diff: -0.00 (SE: 0.25, p = 1.000)

#> Top-All Diff: 3.73 (SE: 1.00, p = 0.000) ***

#>

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

plot(comparison)

Using Subsets

All analysis functions (gates, blp,

clan, gavs, and their comparison versions)

support a subset argument that allows you to evaluate

results on a subset of observations. This is useful when:

- The outcome is only observed for certain observations

- You want to focus on a specific subpopulation

- You need to exclude certain observations from analysis

# Subset with logical vector (e.g., only business owners)

subset_biz <- microcredit$own_anybus == 1

gavs_results <- gavs(pred_fit, n_groups = 3, subset = subset_biz)

# Subset with integer indices

subset_indices <- which(microcredit$lower_window == 1)

gates_results <- gates(fit, n_groups = 3, subset = subset_indices)

# Explicitly use all observations

blp_results <- blp(fit, subset = "all")Important notes: - For gates() and

blp(), the subset must include observations from both

treatment and control groups - For gavs(), this is useful

when outcomes are only observed for certain units (e.g., treatment

effects on outcomes only observable under treatment) - When using

subset, the group_on argument controls which

observations define the group cutoffs. The default

(group_on = "auto") uses the same population that was used

to train the ML model: all observations for

ensemble_hte fits, or the train_idx subset for

ensemble_pred fits trained on a subset. Set

group_on = "all" to always use all observations, or

group_on = "analysis" to form groups within the analysis

subset. The same applies to gates_restricted() and

gavs_restricted(). - A message will be printed indicating

how many observations are used when a subset is applied

Tips and Best Practices

- Number of algorithms: Start with 2-4 diverse algorithms

- Number of folds: K=3 or K=4 recommended

- Number of groups: J=3 (terciles) is standard

- Repetitions: M=5-10 for exploration, M>=100 for final results

- Sample size: Works best with n > 200

Panel Data

For panel or longitudinal data (multiple observations per

individual), use the individual_id argument. This ensures

proper fold splitting (all observations for an individual stay in the

same fold) and uses cluster-robust standard errors. The

microcredit dataset is cross-sectional, so this example

uses simulated data:

# Simulate panel data: 200 individuals x 4 periods

set.seed(123)

N <- 200; T_periods <- 4

panel_data <- data.frame(

id = rep(1:N, each = T_periods),

period = rep(1:T_periods, times = N),

D = rep(rbinom(N, 1, 0.5), each = T_periods),

X1 = rnorm(N * T_periods),

X2 = rnorm(N * T_periods)

)

panel_data$Y <- 2 + panel_data$D * (1 + panel_data$X1) +

0.5 * panel_data$X2 + rnorm(N * T_periods)

# Fit with individual_id for cluster-aware cross-fitting

fit <- ensemble_hte(

Y = "Y",

D = "D",

X = c("X1", "X2"),

data = panel_data,

individual_id = "id",

algorithms = c("lm", "grf"),

M = 10, K = 3

)

# All downstream analyses automatically use clustered SEs

gates(fit, n_groups = 3)

blp(fit)

clan(fit)See the complete guide vignette for a full panel data example.

Performance Tips

Computation time scales with M * K * length(algorithms).

Some guidelines:

-

Debugging: Use

M = 2,K = 3, and 1-2 algorithms to verify your code quickly -

Exploration: Use

M = 5-10with your full algorithm set -

Final results: Use

M >= 100for valid inference (this is required by the methodology) -

Parallelization: Set

n_cores > 1to run repetitions in parallel -

Tuning:

tune = TRUEsignificantly increases time; use only for final results

References

Fava, B. (2025). Training and Testing with Multiple Splits: A Central Limit Theorem for Split-Sample Estimators. arXiv preprint arXiv:2511.04957.

Getting Help

- See

?ensemble_hteand?gatesfor detailed function documentation - Report issues at: https://github.com/bfava/ensembleHTE/issues